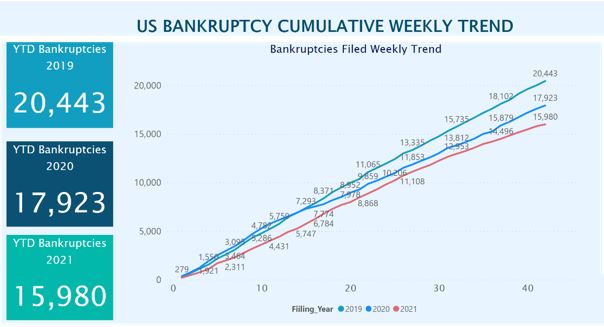

Business bankruptcies continue to slow in 2021

As we begin to close out 2021, here at Dun & Bradstreet we continue to observe economic improvements - despite the many news stories expressing sentiment about global economic struggles and the anticipated rise in bankruptcies and business risk.

For instance, US business bankruptcy trends from 2019 through this year show fewer bankruptcies than some had forecasted (see chart below), as companies encountered and operated with the challenges of the COVID-19 pandemic. US bankruptcies continue to trail behind the pace established in 2019 and have declined consistently over the past three years, building optimism that the commercial community is resilient and will continue to thrive as we move to 2022 and beyond.

(Source: Dun & Bradstreet)

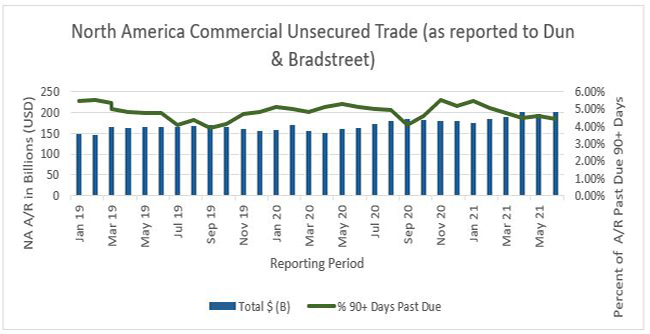

Further, we are beginning to see businesses reengage after the disruption caused by the pandemic. Trade payments (financing done via trade credit) can provide additional insight into understanding the ebbs and flows of the economy. This invoice-based billing is a form of invisible short-term lending that can provide meaningful signals into economic strength.

For example, the chart above shows total balances and percentage past due 90 days as reported by the participating companies in Dun & Bradstreet’s Global Trade Exchange Program, which facilitates the exchange of trade credit experiences allowing a network of data contributors to share accounts receivable data with the business community.

As you can see, delinquency rates (payments that are more than 90 days past due – the green line) began to rise in October 2019 and continued to do so through July 2020 as shown below. That means delinquency rates – those companies that were not paying their bills on time – started rising prior to the onset of COVID-19, and they have continued to come down in 2021, indicating economic recovery.

In parallel, total accounts receivable (as represented in the blue bars) slowed in 2020 as commercial activities were limited to essential activity. The commercial exchange seemed to mirror consumer confidence and illustrated business obligations to control expenses while the future remained unclear.

As we look toward Q3 and the beginning of the fourth quarter of 2021, our data is forecasting continued increases in total invoices and the goods associated with the billings between companies. This is coupled with sustained reduction in overall past due balances. This trend is holding true across all industries worldwide.

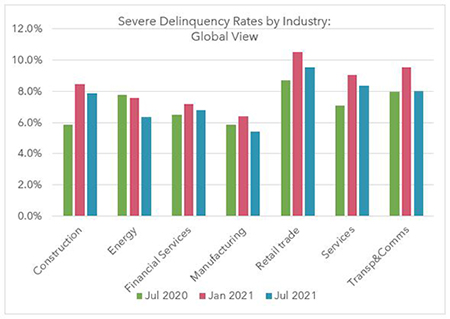

Economic Recovery Not Just a US Phenomenon

These macroeconomic trends that contradict headlines about business-related doom and gloom aren’t just a US phenomenon. The chart below shows that global delinquency rates peaked in January 2021 (the red bars) but are now stabilizing across all industries.

The current outlook continues to be optimistic as we move into the end of 2021 and into 2022 with commercial activity returning at a rapid clip to take advantage of the pent-up consumer demand. In this pursuit of consumer demand, the recovery is maturing in its progression creating pockets of uncertainty. The next challenge many of these businesses will face is how to maintain a robust supply chain in the face of rebounding commercial opportunities.

So, as you can see, the data indicates that while outstanding accounts receivable took a hit during the pandemic as trade credit and other types of lending constricted (and more companies were unable to pay their bills on time) – things are improving. I surmise we are over the hump, and fellow credit and A/R professionals can begin thinking about increasing their risk tolerance in the face of this economic recovery.

Key Takeaways for Changing Credit and A/R Strategies

I’m advising our clients to re-evaluate their company's credit and collections policies to ensure they are:

Accelerating Requests for Credit Limit Increases – Businesses should remain optimistic and anticipate accelerating requests for credit limit increases. Use this opportunity to realign credit limits, and make sure they are informed by the credit exposure you have for the entire global corporate hierarchy.

Actively Respond to Delinquent Accounts – Credit practitioners should actively respond to accounts showing increases in delinquency or lagging payment patterns, as this behavior is contradictory to the current market observations.

Monitoring Portfolio Risk – Portfolio health should be trending less risky and deviations should be monitored closely. Leveraging Dun & Bradstreet predictors such as the D&B Delinquency Score and the D&B Failure Score to monitor your customer portfolio would be beneficial as they have steadily depicted risk throughout the pandemic.

Establishing Appropriate Terms – Evaluating the potential risk of each new opportunity or customer renewal will help realign your credit terms based on the probability the customer will pay on time and within terms, thus helping your company’s cash flow.

Dun & Bradstreet is market leader in data collection and analytics with a robust portfolio of solutions for helping businesses navigate a complex and changing environment. Contact AnalyticsInquiries@dnb.com for information on how we can help you apply this insight.