The Top Ten Global Risks for Businesses

The Dun & Bradstreet Global Risk Matrix (GRM) ranks the biggest threats to business based on each risk scenario’s potential impact on companies, assigning a score to each risk. The scores from the top ten risks are used to calculate an overall Global Business Impact (GBI) score.

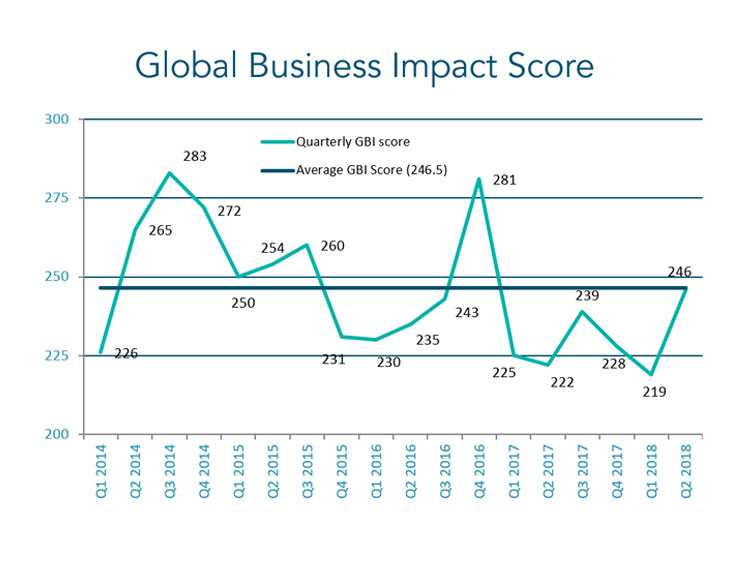

Our latest GBI score highlights a worsening risk outlook for cross-border businesses. This reverses the improving trend seen in the previous two quarters, taking risk to its highest level since Q4 2016, and to just below the long-term average.

Risks at Highest Level Since Q4 2016

Dun & Bradstreet’s GBI score increased from Q1 2018’s record low of 219 (out of a maximum 1,000) to 246 in Q2 2018, indicating a worsening in the global business operating environment. The Q2 score is the highest since the spike of 281 in Q4 2016 and just marginally below the long-term average of 246.5; it is just above the average for 2017 of 228.5.

Our top ten risks combine an assessment of: (i) the magnitude of the event’s probable effect on the global business operating environment, on a scale of 1 to 5 (where 1 is the smallest impact and 5 is the largest); and (ii) the likelihood of the event happening.

Six New Risks in the Global Top Ten

The worsening and more volatile global business operating environment is reflected in six new entries in Dun & Bradstreet’s Q2 2018 Global Risk Matrix: two from North America, two pan-regional, one from West and Central Europe, and the other from Latin America.

The six new-entry risks are:

- US fiscal stimulus leads to overheating. Wages and prices accelerate, the Fed reacts by hiking interest rates faster, and financial stress spikes, triggering a US downturn and choking global growth (GBI 40, out of a maximum 100).

- Growing global debt allied with rising interest rates triggers a fresh debt crisis, creating a systemic banking crisis and sending the global economy into contraction (GBI of 25).

- The boost from the US fiscal stimulus fizzles beyond the near term, but adds to longer-run fiscal and trade deficits, constraining the government’s ability to respond to the next cyclical crisis. This exacerbates the next global slowdown (GBI of 24).

- A right-wing candidate’s victory in Colombia’s presidential election derails the FARC peace process and halts negotiations. This leads to a resurgence of FARC activity and attacks, particularly on oil infrastructure, pushing up global oil prices (GBI of 22).

- Negotiations fail to stop a US-China trade war, which spirals; negative secondary effects offset new opportunities, cooling global trade growth (GBI of 21).

- The speed of monetary loosening in the euro zone is too high, reducing the region’s growth potential – and by extension global growth (GBI of 18).

Among our pre-existing risks, three are unchanged. The GBI of just one risk has increased: this relates to the possibility of Mexico’s resistance to the US’s proposals for the automotive sector pushing final agreement on a revised NAFTA to Q4, thus keeping investor uncertainty heightened and adding to market volatility and, by extension, global uncertainty. Overall, risks remain geographically spread and diverse around new technology, politics, security and policymakers’ actions and reactions to economic developments. This reinforces the notion that finance, procurement and supply chain teams across all business sectors have to combat the impacts of an increasingly complex and globalised world.

Policymakers are Vital to Containing Risk

According to Dun & Bradstreet’s Q2 2018 Global Risk Matrix the actions of policy-makers over the next few months will be crucial for the global business operating environment. In North America, controlling the fiscal stimulus will be vital, as indicated by two of our top four risks. In first place, with a GBI of 40, is our concern that the US fiscal stimulus leads to overheating, heralding a consequent slowdown that would in turn impact global economic growth. A longer-term concern occupies fourth place in our top ten, with a GBI of 24; this is the risk that, beyond the short term, the fiscal boost will merely add to US fiscal and trade deficits, hindering the authorities’ abilities to react to the next cyclic downswing, again impacting global prospects.

Concerns around trade negotiations also feature strongly in the Global Risk Matrix. In equal fifth place with a GBI of 22 (up from 20 in the previous quarter) is the short-term fear that Mexico’s resistance to America’s proposals regarding the automotive sector pushes final agreement on a revised NAFTA to Q4, thus keeping investor uncertainty heightened and adding to market volatility and – by extension – global uncertainty. In addition, we are concerned that negotiations fail to stop a US-China trade war, which spirals, with negative secondary effects offsetting new opportunities and cooling global trade growth; this risk has a GBI of 21 and is seventh place.

Another policy-making environment issue is how the authorities react to the increasing global debt burden, which threatens to trigger another banking sector crisis (which could in turn send the global economy into contraction). This risk is in third place, with a GBI of 25. Finally, in equal ninth place with a GBI of 18 is our concern that the speed of monetary loosening in the euro zone is too high, reducing the region’s growth potential and by extension global growth.

New Technology Causes Uncertainty

Two pan-regional risks relating to technological change again feature in the Q2 2018 Global Risk Matrix. In second place (down from the top position) with a GBI of 36 (the same as the previous quarter) is our concern that the rapidly growing problem of cyber dependence and connectivity will lead to more frequent and more damaging cyber-security issues, with ramifications for doing business; this risk was increasingly evident in 2017. Our second pan-regional technology-related risk is in equal ninth place, with a GBI of 18 (the same as the previous quarter). This cybersecurity risk is related to the accelerated integration of bitcoin and other cryptocurrencies into mainstream global financial transactions and markets, posing new regulatory challenges and risks to investors’ portfolios.

Security Risks Increase in Impact

In equal fifth place, with a GBI of 22, is our worry that a right-wing candidate’s victory in Colombia’s presidential election derails the FARC peace process and halts negotiations, and that this leads to a resurgence of FARC activity and attacks, particularly on oil infrastructure, pushing up global oil prices. Security concerns are also reflected in our worry about an escalation in Iranian-Saudi tensions leading to a direct military confrontation (as opposed to the proxy wars currently being fought). Any direct military conflict would likely target oil installations, pushing oil prices up to at least USD150 per barrel; this risk is in the eighth place with a GBI of 20 (the same as the previous quarter).

Summary: Worsening Risks Highlight Need for Increased Vigilance

The Dun & Bradstreet Global Business Impact score for Q2 2018 shows that risks facing businesses have worsened since the record low experienced in the previous quarter. The score highlights that, despite the improved global economic performance, business decision-makers need to monitor the global business environment continually and carefully. The geographical spread and diversity of risks around new technology, politics, security and policy-making all combine to ensure that the business environment remains challenging.