Understanding Beneficial Ownership Structures

Beneficial ownership identification and verification is now an essential component of the client KYC onboarding and remediation process. It is at the heart of the latest raft of international AML/CTF sanctions and regulations, as well as tax compliance laws and standards, such as FATCA and CRS. Although the impact on the financial services industry is widely acknowledged, other organizations with know your vendor (KYV) and know your third party (KYTP) disclosure obligations are also directly affected.

Scandals such as the Panama Papers, Unaoil, and VimpelCom not only highlight the absolute need for robust customer due diligence (CDD), but have spurred the regulatory momentum for enhanced ownership disclosure and transparency. Failure to comply with the new, stricter regime carries significant reputational and financial risk for both corporations and individuals.

But while the penalties are clearly identifiable, peeling back the complex legal structures designed to conceal Ultimate Beneficial Ownership (UBO) represents a significant challenge. Confusion over multiple beneficial ownership definitions, a lack of accurate ownership registries, disclosure fatigue, and deliberate non-cooperation are additional hurdles.

This guide will help you better understand beneficial ownership legal structures and their complexities. It will also demonstrate how data and analytics can help improve the speed and accuracy of UBO identification, in addition to offering wider organizational benefits from enhanced knowledge management to resource redeployment.

What is Benificial Ownership & Related Concepts

A beneficial owner is defined as the natural person(s) who ultimately owns or controls a customer and/or the natural person on whose behalf a transaction is being conducted. It also includes those persons who exercise ultimate effective control over a legal person or arrangement.

With millions of new companies being registered annually around the world, often with little information required, the sheer scale of identifying an organization’s true owner cannot be underestimated. Complex ownership structures, such as nominee shareholders, and the existence of high-secrecy jurisdictions, such as US shell corporation capitals in Nevada, Wyoming, and Delaware (and the Cayman Islands) only further complicate beneficial ownership identification and verification. Although the role of offshore tax centers was already the subject of public outrage following more than a decade of corporate and public official scandals, it took the publication of the now notorious Panama Papers to demonstrate how flexible offshore legal structures, and the protection offered by offshore jurisdictions, significantly complicate beneficial ownership and UBO identification.

To date, few jurisdictions have defined beneficial ownership, its scope, or threshold. Further, while the numerous AML/CTF regulations and standards largely agree on a definition based on the G20/OECD/FATF principles, each has their own distinct thresholds – meaning that organizations have multiple beneficial ownership compliance initiatives to manage.

But beneficial ownership disclosure is nothing new. Legal frameworks governing the disclosure of ownership and control structures have long existed to ensure the prevention and detection of fraud, corruption, tax evasion, and criminal activity. Although most customers and third parties are legitimate well-run businesses, global terrorist events and geopolitical instability have exposed how terrorists, traffickers, and corrupt officials are funding themselves through financial networks. In response, governments and regulators have recently intensified their efforts to root out financial support to these criminals by requiring organizations to find out who really owns the businesses they deal with and ensure they are trustworthy.

Key Beneficial Ownership Thresholds

FATCA- a 10% ownership threshold or below for Foreign Investment Vehicles

CRS- a 10% ownership threshold

OFAC- 50% rule

High risk or Politically Exposed Persons (PEP) - a threshold as low as 1% or 0.01% is required

FinCEN Final Rule- 25% ownership threshold

4th EU AML Directive - 25% shares or voting rights in a corporate entity. If, after having exhausted all possible means and provided no UBO is identified, the natural person(s) holding the position of senior managing officials are, in principle, considered to be the UBO

Dodd-Frank [sections 13(d) and 13(g)] - beneficial owner of more than 5% of certain equity securities are to disclose information relating to such beneficial ownership

SEC - 506(e) disclosure requires issuers to perform due diligence on any person that is going to become a 20% beneficial owner upon completion of a sale of securities

Regulatory “Catch-22”

It is no secret that the new regulations have created a problematic paradox. The requirement for more granular identification and verification has intensified, but access to information is still limited, and legal concealment strategies are multi-layered and complex. Indeed, beneficial ownership and UBO rely heavily on customer self-certification, as well as information held in company registries and financial institutions, Trust and Company Service Providers (TCSP), regulatory bodies, or authorities.

However, most of these sources have limited or no access to offshore entities or contain unreliable, incomplete data. According to the World Bank, even when public registries do exist, such as the UK’s “Persons of Significant Control” (PSC) register, detailed information on UBO is very rarely included because it is not mandatory. Despite the efforts by governments and regulators to increase transparency and disclosure, information on the UBO of offshore corporate vehicles will not be included in Anti-Money Laundering / Counter-Terrorism Funding central registries.

Overview of The AML/CTF Regulatory Landscape

Guidance - Federal Financial Institutions Examinations Council (FFIEC) Bank Secrecy Act/Anti-Money Laundering (BSA/AML) Examination Manual

International Standards - Financial Action Task Force (FATF), Basel CDD, The Wolfsberg Group, Organization for Economic Cooperation and Development (OECD)

Regulation - 4th EU AML Directive, Persons of Significant Control Register (UK), FCPA/UK anti-bribery laws, Foreign Account Tax Compliance Act (FATCA), US Patriot Act (Title III International Money Laundering Abatement and Anti-Terrorism Financing Act), MiFID II, Market Abuse Directive (MAD II), Solvency II Directive, Financial Crimes Enforcement Network (FinCEN) Final Rule

While there are a raft of different regulations, relying on the one BO definition is not a viable option. For example, the FinCen Final Rule doesn’t require financial institutions to verify that the individuals listed as beneficial owners on self-certification were actually owners of the legal entity.

Without taking further steps to verify beneficial ownership, financial institutions may not be fully compliant with laws implemented in other jurisdictions, such as the 4th EU AML Directive.

Top 7 Beneficial Ownership Challenges

- The Benificial Ownership collection process adds a huge burden on the business’s operations

- The lack of publicly available UBO registry data remains a loophole in the entire AML effort

- Complexity and broadness of the BO data is becoming one of the biggest challenges facing companies with a global footprint in all their markets.

- Non-standard documentation in offshore financial centers (OFCs)

- Flexible change of ownership in OFCs

- Navigating multiple layers of ownership

- Non-cooperation, grudging, or boilerplate disclosure

Adopting a Risk-based Approach to Beneficial Ownership

As a consequence of the changing regulatory landscape, coupled with the challenging nature of available information, UBO identification may seem an insurmountable task. It is usual practice for compliance teams to adopt a risk-based approach with standard thresholds for UBO identification and three lines of defense strategies so as to support straight through processing of business entities with limited risk. As a rule, beneficial ownership falls into three categories: executive directors (and/or senior officers), substantial shareholders (min 3% of an organization’s securities) and de facto third-party shareholders. Calculating UBO is relatively straightforward for a publicly listed company with direct shareholders; it becomes more complex when ownership is obscured by layers of indirect ownership. These ownership structures present high levels of risk and, therefore, require greater scrutiny by compliance teams to demonstrate all reasonable measures have been taken to identify UBO.

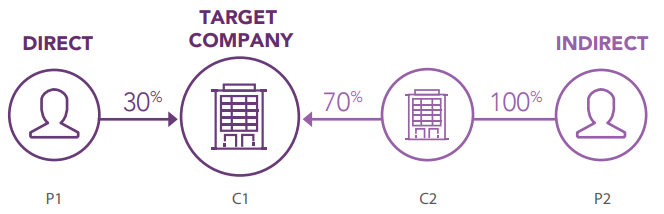

Direct and Indirect Ownership: Connecting the Dots

Beneficial Ownership is best visualized as a series of direct or indirect relationships. In the following diagrams, we have indicated levels of ownership between shareholders and the entities. While direct relationships are straightforward, the indirect relationship can equally be simplistic in its linkage. But in reality, complex structures are more common and granular in detail.

In this example, Person P1 is a direct owner of Company C1 and owns 30% shareholding. Person P2 is an indirect owner of Company C1 and owns 70% shareholding.

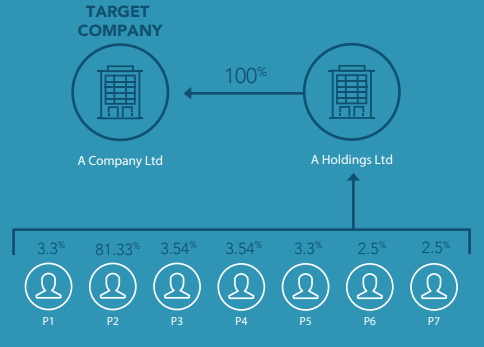

Simple Indirect Shareholding

This diagram visualizes a typical scenario depicting how organizations determine the UBO of a target business. In this instance, the shares are owned by multiple people. In this example, Person 2 has 81.33% ownership of A Holding Ltd. The level of ownership an organization wants to work with and build into its thresholds comes down to an individual risk-based approach and risk appetite. What robust beneficial ownership identification requires is reliable, and when necessary, granular investigation.

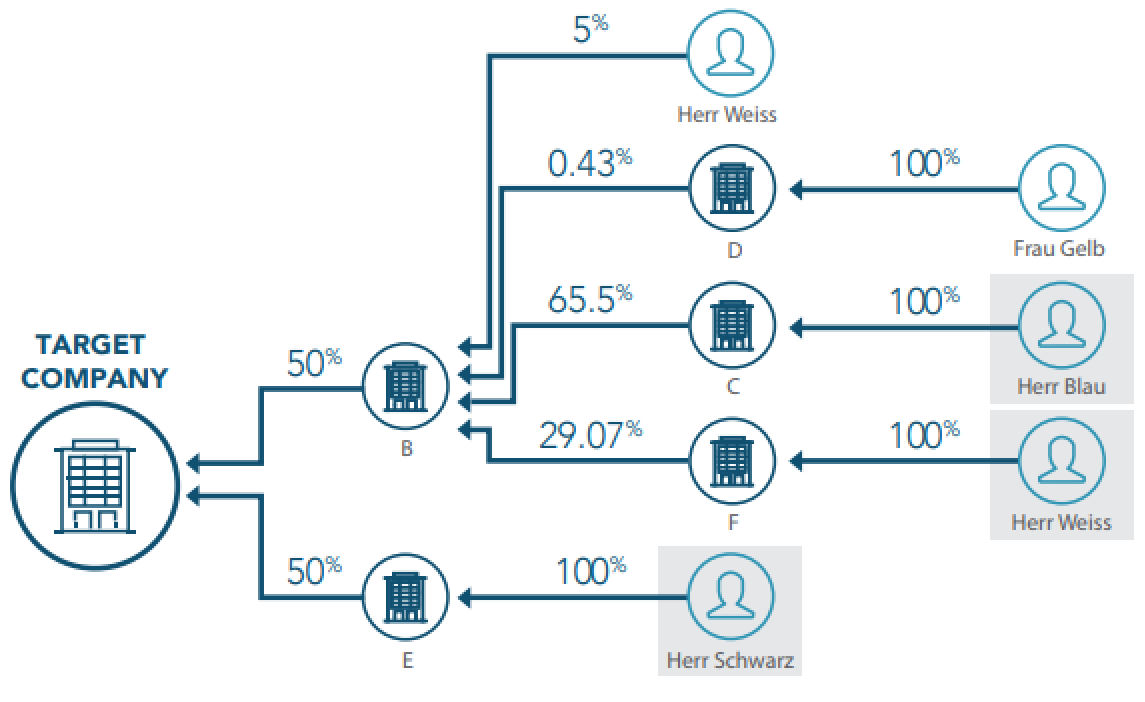

Multi-Level Indirect Shareholding

In this scenario, there are multiple levels of indirect ownership. The three beneficiaries are clearly marked in grey boxes. In this case, Herr Blau has a 32% interest in target company A (50% x 65% = 32%), Herr Weiss has 14%, and Herr Schwarz has 50%. Note that Herr Weiss has both a direct and indirect interest in Company B.

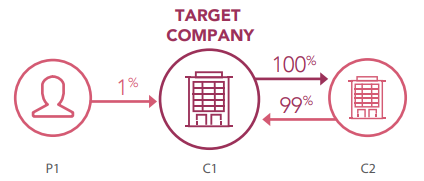

Looping Relationships (multi-level indirect shareholding )

In this scenario, for example, we have a seemingly unimportant 1% owner. In reality, this individual is the only UBO, with all the profits being delivered to the UBO in 1% shares. For example, if the company makes a $10 profit, the UBO will receive full profit, but in 1% increments.

Corporate structure vehicles exist to enable organizations to create a loop in which they own holdings of other companies in the same loop, as well as potentially shares in themselves.

By tallying the ownership percentage of each company, most but not all organizations in the loop will derive 100% of their ownership entirely from other companies (not individuals) in the loop. Where they don’t, the shortfall represents the percentage that the shareholder registry states are owned by individuals. These quoted percentages will be lower than what the individuals actually own and control if they’re the only people associated with the loop.

A Data-Inspired Approach to Calculating Ultimate Beneficial Ownership

For many organizations, getting to the detail is not straightforward. Typically, it can take days to manually identify attributes (confirming self-certified information such as company name, address, registration details), verify those attributes (such as ownership levels and financial reports), and, if deemed necessary, conduct EDD. To calculate ultimate beneficial ownership, compliance teams often working in silos and — in different jurisdictions — have to rely on multiple reports and spreadsheets, as well as a range of online business information reports. These reports are inflexible, potentially inaccurate, and do not necessarily integrate with other systems and data sources. And of course, the structure can shift quickly, with small changes in one part affecting the whole.

For example, applying a traditional approach to corporate linkage to the multiple-level indirect shareholding scenario would fail, since there are two entities that have an equal 50% share rather than a single global parent. To be able to accurately verify and calculate the actual ownership, it is essential that accessible data pulls together global corporate linkage and personal share ownership. This can be achieved by harnessing data and analytics to automate the identification and verification of beneficial ownership.

By far the most common approach is to bring workflow and content together through Application Programming Interface (API) technology. This dramatically accelerates the data capture process and ensures workflows can be built as needed, enabling straight through-processing where possible and directing complex remediation to the right teams quickly. Instead of using online business information reports and spreadsheets to calculate ultimate beneficial ownership, the analyst makes a query on the business entity in question via the API. This triggers analysis of the direct, indirect, and circular ownership structures of the business entity, and delivers back within seconds the relevant shareholders and their percentage ownership stakes. It also supports the building of an alerts methodology for changes to ownership. By breaking the remediation cycle and reacting to changes immediately, valuable resources can focus on the right customers, assessing changes that matter and acknowledging those that are not of material concern.

The ability to identify beneficial owners in a few clicks not only helps fast-track the standard onboarding process, but frees up internal resources to focus on more complex investigations. Furthermore, by delivering this data into a central data repository and utilizing visualization software, other business units are able to access the same information, creating a relationship data supply chain that can expedite decisionmaking and organizational efficiency. Migrating to a data-inspired approach offers other value-added benefits too. In addition to reducing exposure to reputational risk (such as screening for potentially damaging PEPs), businesses can eliminate manual entry errors, enhance enterprise-wide knowledge management, and increase sector competitiveness and business agility while reducing operational costs.

Determining Beneficial Ownership Recommendations

E Start small – Look at entities that have been sold higher-risk products and remediate them with data that can be consumed in bulk and stored locally, solving any immediate challenges

E Use API technology to build straight-through processes for new onboarding or KYC

Embrace the power-of-change detection within a target entity or in entities associated in a beneficial ownership structure. Alerts recommending a re-run on a customer can minimize the effort of full reviews. Reacting to change immediately means far less effort down the line

Easing the Pain of Beneficial Ownership Identification with Data

There is little doubt that confusion over multiple beneficial ownership definitions, a lack of public ownership registries, disclosure fatigue, and deliberate non-cooperation represent significant challenges to organizations affected by AML/CTF regulations. The globalization of beneficial ownership aided by the complexity of legal corporate vehicles and the use of offshore financial centers requires a forensic examination of data collected from multiple jurisdictions. For now, transparency over ultimate beneficial ownership is still the exception, not the rule, in many jurisdictions.

But even though the challenges are significant, data analytics is significantly easing the pain of beneficial ownership identification. By harnessing technology and exploiting on-demand, timely, accurate, and reliable data sources that pull together global corporate linkage on business entities and personal share ownership, organizations can be confident that they have achieved the single customer view they need to meet compliance challenges and mitigate reputational risk.

Ultimately however, the advantages of a data-inspired approach can only be achieved by partnering with a trusted third-party data provider that is capable of verifying vast quantities of information acquired through a reliable, transparent data supply chain. While the “all reasonable measures” test is a regulatory minimum standard, relevant and high-quality data that is shared across the enterprise can help organizations move beyond compliance as a box-ticking obligation to become more agile and competitive.